Crypto Tax Calculator 2025

Calculate Your Tax Liability

Determine your capital gains tax under the new 2025 regulations

Tax Breakdown

Important Notes

Under 2025 rules:

- Staking and airdrops are taxed as ordinary income

- Long-term gains (held >1 year) qualify for lower rates

- NFT transactions are taxed at 28%

- High earners (> $200k single) owe additional 3.8% NIIT

The future of cryptocurrency taxation isn’t something you can ignore anymore. If you’ve ever bought, sold, traded, or earned crypto, you’re already part of the system-and the rules changed dramatically in 2025. What used to be a gray area is now a tightly regulated landscape with real consequences for getting it wrong. The IRS isn’t asking nicely anymore. They’re watching. And they’ve got the tools to prove it.

What Changed in 2025? The Big Three

Three major shifts hit crypto taxpayers on January 1, 2025. These aren’t minor tweaks. They’re foundational changes that rewrite how you report your crypto activity.First, Form 1099-DA became mandatory. Every U.S. crypto exchange-Coinbase, Kraken, Binance.US, you name it-must now report every single transaction you make. That includes trades between different coins, staking rewards, airdrops, and even small purchases made with Bitcoin. It’s the same system banks use for stocks. No more guessing what the IRS knows. They’ll have a complete record.

Second, the IRS killed the universal cost basis method. You can no longer average your purchases across all wallets. Now, you must track your cost basis wallet by wallet. If you bought Bitcoin on Coinbase in 2022 and moved it to a Ledger in 2024, then sold it in 2025, you need to know exactly what you paid for it in that specific wallet. No more using a calculator and hoping for the best.

Third, the IRS started requiring detailed records of self-transfers. If you move crypto from one wallet you own to another, you still need to log it. Why? Because future systems will link wallets to track holding periods. Right now, you’re the only one keeping that chain of custody. Miss a transfer, and your long-term gain could become a short-term one-costing you thousands.

How Crypto Gains Are Taxed Now

Crypto isn’t treated like cash. It’s treated like stocks or real estate-property. That means two types of taxes apply, depending on what you did and how long you held it.If you earned crypto as income-through mining, staking, airdrops, or being paid in Bitcoin-it’s taxed as ordinary income. That means it gets added to your salary, and you pay federal rates from 10% to 37%, based on your total income. For 2025, if you’re single and made $75,000 from your job and $10,000 in staking rewards, your total taxable income is $85,000. The staking portion isn’t treated differently. It’s all one pile.

If you sold or traded crypto, you triggered a capital gain or loss. If you held it less than a year, it’s short-term. Same tax rate as your salary. If you held it over a year, you get the lower long-term rate. For 2025, single filers pay 0% on long-term gains if their taxable income is under $48,350. Between $48,351 and $533,400, it’s 15%. Above that, it’s 20%.

But here’s the kicker: if you’re a high earner, you might also owe the Net Investment Income Tax. That’s an extra 3.8% on investment income-including crypto gains-if your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married). So a $100,000 long-term crypto gain could be taxed at 23.8% total, not just 20%.

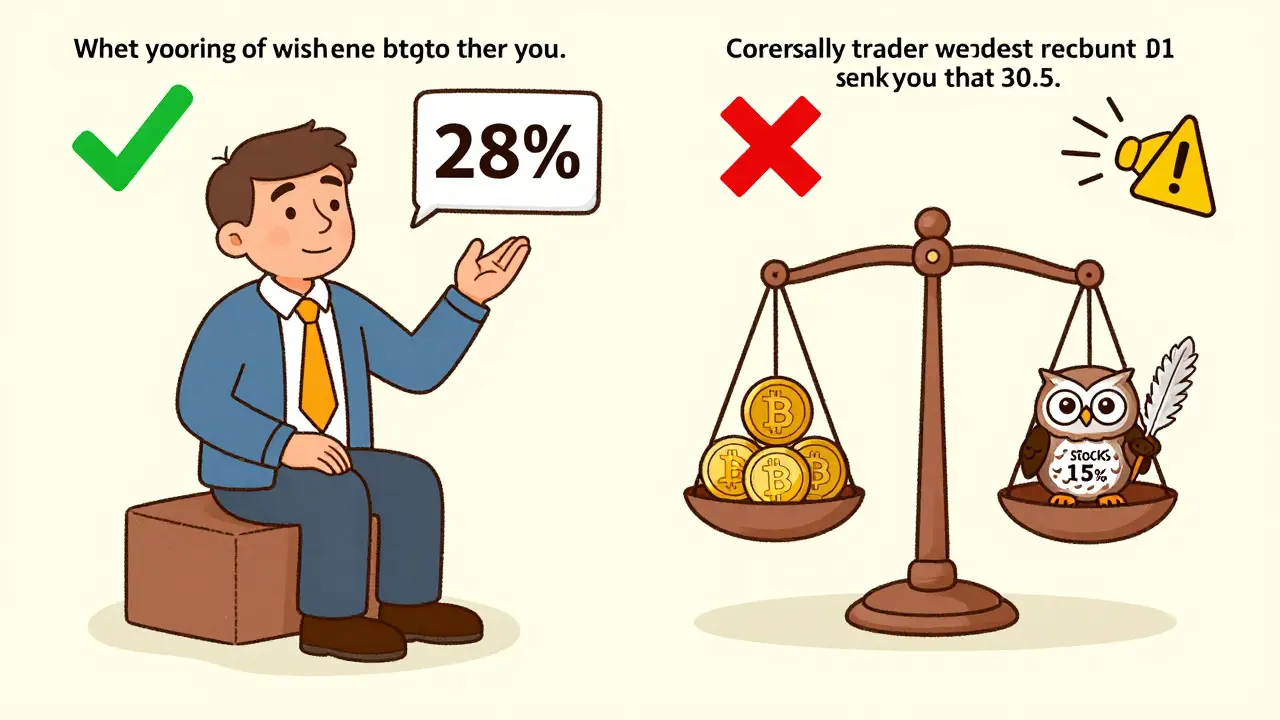

NFTs and Collectibles: The Hidden Trap

Not all crypto is treated the same. NFTs, digital art, and collectible tokens are classified as collectibles under IRS rules. That means even if you held them for five years, your long-term capital gains rate jumps to 28%. No exceptions. No breaks. That’s higher than the top rate for stocks.Imagine you bought an NFT for $5,000 in 2023 and sold it for $50,000 in 2025. Even though you held it over a year, you owe 28% on the $45,000 profit. That’s $12,600 in federal taxes alone. Most people assume NFTs are just like Bitcoin. They’re not. This is a major pitfall.

And it gets worse. Some DeFi tokens that behave like collectibles-like rare in-game items or limited-edition digital assets-could also be classified this way. The IRS hasn’t issued a full list yet. So if you’re trading anything that feels more like a digital trading card than a currency, assume the worst-case tax rate applies.

What’s Coming Next? Wash Sales and More

President Biden’s 2025 budget proposal includes one of the biggest changes yet: applying the wash sale rule to cryptocurrency.Right now, if you sell Bitcoin at a loss and buy it back the next day, you can claim that loss to offset other gains. It’s called tax-loss harvesting. It’s legal. It’s common. It saves people thousands.

Under the new rule, that’s gone. If you sell crypto at a loss and repurchase it within 30 days, you can’t claim the loss. The IRS will treat it like you never sold it. This mirrors how stocks are treated. It’s designed to stop people from gaming the system.

But here’s what most people don’t realize: this rule could hurt long-term investors. Say you’re holding Ethereum and want to rebalance your portfolio. You sell some to buy Solana, then buy back Ethereum a week later because you still believe in it. That’s a normal strategy. Now, you lose the tax benefit. You’ll need to wait 31 days-or accept the higher tax bill.

How to Stay Compliant in 2025

The new rules make DIY tax prep risky. But you don’t need a CPA to survive-if you’re organized.- Track every transaction. Use a crypto tax tool like Koinly, CoinTracker, or ZenLedger. Import your wallet addresses and exchange history. Don’t rely on exchange statements alone-they don’t track self-transfers.

- Separate your wallets. Don’t mix funds from different sources. If you got airdrops in one wallet and bought crypto in another, keep them separate. It makes cost basis tracking easier.

- Save your records. The IRS can audit you for up to six years. Keep transaction IDs, timestamps, wallet addresses, and USD values at time of trade. Screenshots aren’t enough. Use a digital ledger.

- Don’t ignore past years. If you traded crypto before 2025 and didn’t report it, you’re at risk. The IRS now has cross-referenced data from exchanges. Filing amended returns now is cheaper than waiting for a notice.

- Use charitable donations. If you have crypto that’s gone up in value, donate it directly to a qualified charity. You avoid capital gains tax and get a deduction for the full market value. It’s one of the most powerful crypto tax strategies left.

What This Means for You

The future of cryptocurrency taxation isn’t about banning crypto. It’s about bringing it into the same system as stocks, bonds, and real estate. The goal isn’t to punish investors. It’s to make sure everyone pays their fair share.That means more paperwork. More tracking. More stress. But it also means legitimacy. As crypto becomes more mainstream, tax clarity helps institutions, banks, and even governments trust it.

If you’re holding crypto long-term, focus on timing your sales. Use the 0% and 15% brackets wisely. If you’re active trader, prepare for the wash sale rule to force you to slow down. If you’re into NFTs, treat them like collectibles-not investments-and plan for the 28% rate.

2025 isn’t the end of crypto taxation. It’s the beginning of the real one. The rules will keep evolving. But the one thing that won’t change: ignorance is no longer an excuse.

Do I have to pay taxes on crypto I didn’t sell?

Yes. If you earned crypto as income-through staking, mining, airdrops, or being paid in crypto-you owe taxes on its value at the time you received it. Even if you never sold it, the IRS treats it as taxable income. Holding crypto without selling doesn’t make it tax-free.

What happens if I don’t report my crypto transactions?

The IRS now receives Form 1099-DA from exchanges, so unreported crypto is easy to spot. Penalties include interest on unpaid taxes, a 20% accuracy-related penalty, or even criminal charges for intentional evasion. In 2024, the IRS collected over $1.2 billion in crypto-related taxes and penalties. Expect that number to grow in 2025.

Can I use crypto to pay my taxes?

No. The IRS does not accept cryptocurrency as payment for taxes. You must convert your crypto to USD and pay with cash, bank transfer, or credit card. Even if you use a third-party service that claims to pay taxes with crypto, you’re still responsible for reporting the sale as a taxable event.

Are crypto-to-crypto trades still taxable?

Yes. Trading Bitcoin for Ethereum, or Solana for Cardano, is a taxable event. Each trade counts as a sale of the first asset and a purchase of the second. You must calculate the gain or loss on the asset you sold. There is no tax-free exchange rule for crypto like there is for real estate.

Do I need to report small crypto purchases, like buying coffee with Bitcoin?

Yes. Any use of crypto to buy goods or services is a taxable event. If you bought a $50 coffee with Bitcoin you bought for $20, you have a $30 capital gain. This applies regardless of the amount. Most people don’t track this, but the IRS now requires exchanges to report these transactions through Form 1099-DA.

Comments

Jonathan Sundqvist

They’re making it harder just to punish small-time holders. I bought $200 worth of ETH in 2021 and now I’m supposed to track every satoshi like it’s gold? Give me a break.

December 4, 2025 AT 16:08

Jerry Perisho

Form 1099-DA is a game changer. If you’re using multiple wallets and not tracking transfers, you’re already behind. Tools like Koinly automate the worst parts. Just import your keys and walk away.

December 5, 2025 AT 15:57

Adam Bosworth

lol the IRS thinks they can tax digital art like it’s a vintage car. Next they’ll charge me for breathing air that contains blockchain data. This is fascist control disguised as ‘fairness’.

December 5, 2025 AT 22:46

Chloe Hayslett

Oh so now we’re supposed to pay 28% on NFTs but 15% on stocks? Real patriotic. America’s tax code is a circus and crypto’s the clown they picked to beat up.

December 6, 2025 AT 04:29

Isha Kaur

I’m from India and this is wild to read. Here, crypto isn’t even regulated properly, but I see how this level of detail helps prevent fraud. The wallet-by-wallet tracking is brutal but fair. I wish our government would take this seriously.

December 7, 2025 AT 06:50

Renelle Wilson

It’s important to remember that these rules aren’t meant to crush innovation - they’re meant to protect people from themselves. Many investors don’t realize how easily they can get burned by not tracking cost basis. The IRS isn’t the enemy here; ignorance is. If you’re overwhelmed, reach out to a nonprofit tax clinic. They help low-income crypto holders for free.

December 8, 2025 AT 16:45

Krista Hewes

Wait so if I move btc from coinbase to my ledger and then sell it… I need to know what I paid for it on coinbase? What if I forgot? I didn’t even save the receipt. I’m doomed.

December 9, 2025 AT 14:12

Tara Marshall

You’re not doomed. Use blockchain explorers. Paste your old transaction ID and it shows you the purchase price. I’ve done it for 8 years. It’s tedious but doable.

December 10, 2025 AT 17:22

Noriko Robinson

Don’t forget to document your wallet addresses with timestamps. I screenshot every transfer and save it in a folder labeled ‘Crypto Tax Evidence 2024’. It saved me during my audit last year. No one’s coming to help you - you gotta be your own advocate.

December 12, 2025 AT 01:25

Jon Visotzky

So wash sales are coming? That’s gonna mess up so many people’s strategies. I’ve been selling my losers every December to reset. Now I gotta wait 31 days? That’s like forcing me to hold bad investments. What’s the point?

December 13, 2025 AT 16:49

Yzak victor

Bro the wash sale rule is just the IRS saying ‘you can’t outsmart us’. But honestly? It’s fair. If you’re trading like a casino, you shouldn’t get tax breaks. Real investors hold. Period.

December 14, 2025 AT 05:06

Holly Cute

Oh so now I can’t tax-loss harvest? Cool. So the government wants me to pay more tax so they can fund more drones? Thanks, patriots. I’m just gonna burn my Ledger and move to Uruguay. At least there, they don’t care if I trade Dogecoin for avocado toast.

December 14, 2025 AT 22:00

Nelson Issangya

Don’t give up. This is the price of legitimacy. When crypto becomes as normal as stocks, we’ll have pensions, 401ks, and financial advisors who get it. Right now we’re the pioneers. Pain now, comfort later.

December 15, 2025 AT 07:02

Uzoma Jenfrancis

They treat crypto like a threat. But in Nigeria, we use it to survive. Your taxes don’t matter when your currency is collapsing. Why are you forcing your rules on the world?

December 16, 2025 AT 13:21

Manish Yadav

This is why crypto is evil. People lie. People cheat. Now the government is forcing them to be honest. Good. Let them pay. They stole from the system long enough.

December 16, 2025 AT 16:19

ronald dayrit

What does it mean to ‘own’ something when the state can dictate how you account for its value? The moment you must track every movement of your digital asset to appease a bureaucratic apparatus, you no longer own it - you are its custodian under surveillance. The blockchain was supposed to free us from intermediaries. Now the IRS is the ultimate intermediary. We traded one tyranny for another - just with more forms.

December 16, 2025 AT 17:51

Glenn Jones

28% on NFTs? That’s a joke. I bought a pixelated ape for $10k and sold it for $150k. They want $37k in taxes? I’d rather burn the NFT than pay that. And don’t even get me started on how they’ll track crypto-to-crypto trades - they’re gonna need a quantum computer to keep up.

December 18, 2025 AT 16:01

Neal Schechter

Most people don’t realize the charitable donation trick is still alive. I donated 10 ETH last year to a crypto nonprofit. Got a $30k deduction and paid $0 in capital gains. It’s legal. It’s smart. And 90% of people don’t know it exists.

December 20, 2025 AT 10:20

Roseline Stephen

I’ve been holding since 2017. I’ve never reported a single trade. I’m not scared. The IRS has better things to do than chase me. I’ll just keep using my hardware wallet and ignore the news.

December 21, 2025 AT 01:45

Mairead Stiùbhart

Oh wow, so now I can’t sell my BTC at a loss and buy it back tomorrow? That’s like telling a chef they can’t taste their own soup. What’s next? Taxing the joy of trading?

December 22, 2025 AT 18:18

Elizabeth Miranda

It’s not about control. It’s about clarity. For years, people thought crypto was a tax-free zone. It never was. The rules just weren’t enforced. Now they are. That’s progress, not persecution. The real problem is that we never had proper education around it. We got caught flat-footed.

December 24, 2025 AT 05:29

Doreen Ochodo

Track everything. Use Koinly. Donate to charity. Ignore the noise. You got this.

December 24, 2025 AT 22:12

Josh Rivera

Wow. So the IRS is finally treating crypto like real money? Took them long enough. Now let’s tax the miners, shut down the darknet wallets, and make every wallet KYC. Only then will crypto be ‘legit’.

December 26, 2025 AT 03:21

Renelle Wilson

Thank you for saying that. I’ve seen too many people treat this like a game. It’s not. It’s financial responsibility. And yes, it’s a pain - but so is filing W-2s. We’re just leveling up. The next generation won’t even think twice about tracking their crypto. They’ll have apps that do it for them. We’re the dinosaurs.

December 27, 2025 AT 21:06